I was reviewing a client’s books last month when something caught my eye. Their Profit & Loss showed $340,000 in sales for the quarter. Pretty impressive, right?

Except when I looked at their bank statements, only about $180,000 had actually come in.

“Must be a lot of outstanding invoices,” I thought. But when I checked Accounts Receivable, it was nearly empty. So where was the other $160,000?

The answer was hiding in a little account called Undeposited Funds, and it had been quietly inflating their sales numbers for over a year.

What Is Undeposited Funds, Anyway?

If you use QuickBooks or similar accounting software, you’ve probably seen this account lurking in your chart of accounts. It sounds technical and intimidating, so most business owners just… ignore it.

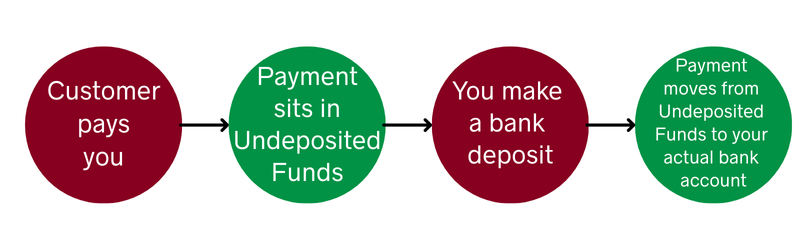

Here’s what it’s supposed to do: act as a temporary holding tank for payments before they’re deposited in the bank. Think of it like the checks sitting on your desk waiting to go to the bank, or the credit card payments that haven’t been batched yet.

Clean, tidy, organized.

Except that’s not what happens in a lot of businesses.

How It Should Be

Step 1: You Send an Invoice

You complete a project and send your client an invoice for $5,000.

The moment you create that invoice in your accounting system, something happens automatically: that $5,000 is recorded as income on your Profit & Loss statement.

You haven’t been paid yet, but accounting-wise, you’ve “earned” that revenue. It also shows up in Accounts Receivable, basically a list of money people owe you.

So far, so good. This is actually correct under accrual accounting.

Step 2: The Payment Arrives

Great news, your client pays! The $5,000 hits your bank account.

Now, here’s where things should happen: you (or your bookkeeper) should go into your accounting system and apply that payment to the open invoice. This tells the system, “Hey, remember that $5,000 we said we earned? Well, we actually got paid for it now.”

When done correctly:

- The $5,000 moves out of Accounts Receivable (because it’s no longer owed to you)

- It goes through Undeposited Funds briefly

- Then it lands in your bank account

- Your income stays at $5,000, counted once, as it should be

What Actually Happens (The Problem)

But here’s what happens in poorly managed books:

Instead of applying the payment to the existing invoice, someone records it as a new deposit directly to income.

So now your accounting system thinks:

- You earned $5,000 when you created the invoice (recorded as income #1)

- You earned another $5,000 when the payment came in (recorded as income #2)

Your books now show $10,000 in sales from a single $5,000 transaction.

Meanwhile, that $5,000 payment is sitting in Undeposited Funds, never properly cleared, and your Accounts Receivable still shows the invoice as unpaid (even though you definitely got paid).

It’s a mess.

Why This Is Such a Big Deal

You might be thinking, “Okay, that sounds annoying, but does it really matter?”

Yes. It really, really matters.

Your Numbers Are Lying to You

When your sales are inflated, you’re making decisions based on fiction.

You look at your P&L and think, “Wow, we had a great quarter! Let’s hire another person,” or “Revenue is up, time to invest in that new equipment.”

But then you look at your bank account and think, “Wait, where’s all that money?”

The cognitive dissonance is real. You feel like you should be doing well because your reports say you are, but you’re stressed about cash and can’t figure out why.

You’re Potentially Overpaying Taxes

Here’s a fun one: if your sales are doubled on paper, you might be paying taxes on income you never actually received.

Depending on your accounting method and when you file, this could mean writing a check to the IRS for phantom revenue.

I once worked with a client who had overpaid about $18,000 in taxes over two years because their sales were consistently overstated. When we finally cleaned up their books, we had to amend returns and go through a whole process to get that money back.

Not fun.

You Look Unreliable to Others

If you ever need a loan, bring in an investor, or sell your business, people are going to look at your financials.

If your books are a disaster, especially if your reported revenue doesn’t match your bank deposits, you immediately lose credibility. Lenders get nervous. Investors walk away. Buyers lowball you or disappear entirely.

Even if you’re not doing anything intentionally wrong, messy books make you look either incompetent or dishonest. Neither is a good look.

The IRS Might Come Knocking

Inaccurate financial reporting isn’t just embarrassing; it can trigger audits.

If your tax returns show revenue that doesn’t align with your actual bank deposits, that’s a red flag. The IRS might start asking questions. And once they’re asking questions, you’re in for months of stress, professional fees, and documentation headaches.

Even if everything gets resolved in your favor eventually, it’s a nightmare you don’t want.

How to Tell If You’re in This Trap

Okay, so how do you know if this is happening to you?

Red Flag #1: Your Undeposited Funds Account Has a Balance

Pull up your chart of accounts and review the Undeposited Funds account. Does it have a balance?

If the answer is yes, especially if it’s a large balance or it’s been sitting there for months, you’ve got a problem.

Undeposited Funds should be essentially empty most of the time. Money should flow through it quickly (like within days) and then be transferred to your bank account.

If it’s become a permanent resident? That’s your first clue.

Red Flag #2: Sales Look High, But Cash Feels Low

You run your P&L and think, “Okay, we made $80,000 last month, that’s solid.”

But then you look at your bank balance, and it doesn’t feel like you made $80,000. Where did it all go?

If you’re consistently confused about why your revenue numbers don’t match your actual cash position (and you’re not carrying a ton of receivables), doubled income might be the culprit.

Red Flag #3: Customer Payments Don’t Match Open Invoices

Let’s say a customer paid you three weeks ago, and you saw the money hit your account. But when you look at your Accounts Receivable report, their invoice still shows as unpaid.

That’s because the payment was recorded as new income instead of being applied to the existing invoice.

Red Flag #4: Your Books Reconcile, But Something Still Feels Off

Here’s a tricky one: sometimes your bank reconciliation looks perfect. Everything matches. Your bookkeeper gives you a thumbs up.

But you still have that nagging feeling that something isn’t right. The numbers just don’t feel accurate.

Trust that instinct. Just because your bank rec balances doesn’t mean your income is recorded correctly.

How to Fix It If You’re Already in This Mess

If you’ve realized you have a problem, don’t panic. It’s fixable, but it does require going back and cleaning things up properly.

Step 1: Stop the Bleeding

First things first: stop recording new transactions the wrong way.

Make sure anyone handling your books understands the correct process. Every payment needs to be applied to its corresponding invoice, not recorded as new income.

Step 2: Reconcile Your Undeposited Funds

Go through that Undeposited Funds account line by line. Each entry should correspond to a real payment that either:

- Needs to be deposited, or

- Was already deposited but never properly cleared

Match them up with your bank deposits and clean them out.

Step 3: Review and Correct Doubled Income

This is the tedious part. You’ll need to go through your income transactions and identify which ones were recorded twice.

For each doubled transaction:

- Keep the original invoice/income entry

- Delete or reverse the duplicate deposit

- Make sure the payment is properly applied to the invoice

Step 4: Review Your Accounts Receivable

Once you’ve cleaned up the income side, check your Accounts Receivable aging report. Make sure:

- Paid invoices are marked as paid

- Unpaid invoices actually haven’t been paid yet

- Nothing is sitting there incorrectly

Step 5: Reconcile Everything

After you’ve made corrections, reconcile your accounts again to make sure everything balances.

Your P&L should now show accurate sales numbers, your Undeposited Funds should be (mostly) empty, and your Accounts Receivable should only show legitimately unpaid invoices.

Preventing This From Happening Again

Once you’ve cleaned things up, here’s how to make sure it doesn’t happen again:

- Train everyone properly. Anyone who touches your books needs to understand the correct process for receiving and recording payments.

- Use your accounting software correctly. Most systems have a “Receive Payment” function that’s separate from “Make Deposit.” Use them in the right order.

- Review Undeposited Funds regularly. Make it a habit to check this account weekly. If anything’s been sitting there more than a few days, investigate why.

- Reconcile more than just your bank account. Yes, your bank rec needs to balance, but also regularly review your P&L, Accounts Receivable, and other key reports to make sure they make sense.

- Work with a professional. If bookkeeping isn’t your thing (and honestly, it shouldn’t be), hire someone who actually knows what they’re doing, not just someone who “knows QuickBooks.”

The Bottom Line

Accurate sales reporting is the foundation of every good business decision you make.

If your books are telling you that you’re making more money than you actually are, everything falls apart. You can’t plan properly. You can’t manage cash flow. You can’t grow strategically.

And in the worst cases, you end up overpaying taxes, losing credibility with lenders or investors, or even facing IRS scrutiny.

The Undeposited Funds trap is one of those invisible problems that can quietly wreck your financial clarity for months or years before you realize it’s happening.

But here’s the good news: it’s completely preventable and fixable if you catch it early.

So, take a minute today. Open up your accounting software. Look at that Undeposited Funds account.

If there’s a balance sitting there, it’s time to dig in and figure out what’s really going on.

Because you deserve to know the truth about your business, not a fiction that’s been quietly inflating your sales numbers while leaving you confused about where all the money went.

Need Help Cleaning Up Your Books?

If you’re looking at your Undeposited Funds account right now and feeling overwhelmed, we can help.

Our Free Financial Cleanup & Accuracy Review includes:

- Complete analysis of your Undeposited Funds and payment recording

- Identification and correction of doubled income entries

- Accounts Receivable reconciliation

- Training for your team on proper procedures

- Systems to prevent future issues

Let’s uncover what your numbers are really saying, and make sure they’re telling you the truth.

Schedule Your Financial Review

About Fruitful Enterprises: We help business owners gain confidence in their numbers through accurate bookkeeping, smart systems, and strategic financial guidance. Your books should clarify your business, not confuse it.